It wouldn’t be wrong to say that the second-most populous country in the world is using mobile phones to the best of its abilities. Considering the fact that the country is also the second-largest consumer of smartphones in the world, its government is exploiting this opportunity for realising its dream of making India a Cashless economy. It is doing this through the use of mobile phone-enabled UPI.

UPI or Unified Payment Interface is a term that almost the whole of India is now familiar with. Its existence has made the life of Indians hassle-free. Now, one no longer needs to wait in long queues for transferring money from one account to another, or for withdrawing money to pay someone in cash. One also doesn’t need to wait for a cheque to get cleared in order to make timely payments. All of this is now done through a UPI mobile application.

What is UPI or Unified Payment Interface?

It is an interface, a single platform, that merges various banking services to simplify almost all kinds of transactions between individuals and businesses/institutions. UPI, in simple words, is a payment model that lets anyone with a smartphone make payments easily and instantly.

When did UPI come into being?

UPI was developed in 2016 by NPCI or National Payments Corporation of India ( a body set up by RBI and the Union Finance Ministry in 2009 to regulate retail payments and settlement systems in India.) It was launched after demonetisation was executed by the Modi Government in an attempt to make India a digital economy and fight black money and corruption.

NCPI developed UPI with the main objective of simplifying digital transactions and providing a single interface which could be utilised across all systems.

What are some common benefits offered by UPI?

- It is speedy. Money can be transferred from one bank account to the other within seconds.

- It is accessible to a wider audience in India who own a smartphone. It does away with the need to visit your bank for basic banking activities like depositing a cheque.

- The platform is a multipurpose application which also enables users to pay their bills, book tickets, etc.

- You do not need to carry cash or debit/credit card while stepping out to buy anything. Just your smartphone is enough to make any kind of purchase.

- UPI enables you to make payments with the help of only a contact number of the one you want to make the payment to, a Quick Response (QR) code or a UPI id. You do not need to enter any bank details like bank account number, name of the account holder, IFSC code, bank branch, etc.

- The daily transaction limit is Rs 1 lakh. Unlike the banks that require you to provide details of your PAN (Permanent Account Number) for making payments above Rs 50,000, UPI doesn’t have any such requirement.

- To make a payment, you only need to enter your UPI pin to authenticate the transaction.

What kind of reach does UPI have?

The kind of reach that UPI is having in India is stupendous. According to India Digital Payments Report 2020 released by Worldline, the top 10 states with the most UPI transactions were Maharashtra, Karnataka, Tamil Nadu, Kerala, Andhra Pradesh, Delhi, Uttar Pradesh, Gujarat, West Bengal and Telangana. Similarly, the top 10 cities include Bengaluru, Chennai, Mumbai, Hyderabad, Pune, Delhi, Coimbatore, Kolkata, Ernakulam and Ahmedabad.

In the initial stages, what started out as a P2P (person to person) payment mode gradually evolved into becoming a preferred merchant payment platform (P2M). Now, UPI has a P2M (person to merchant) market share volume of 41 per cent.

Indian beggars using UPI to collect alms speak widely about the massive success UPI is having in the country, to say the least. Today, even the smallest stalls use UPI as a payment method. Right from e-commerce applications like Amazon, Nykaa, Zomato, Dunzo, physical grocery stores, fuel stations, clothing and apparel, pharmacies, and restaurants to local vegetable vendors and roadside tea sellers located in even the most remote/rural area in India are using UPI.

How does UPI operate?

It is extremely easy to use UPI. It primarily requires a mobile number registered with your bank account or a UPI id to make and receive payments. To start using UPI, you must first create a UPI id and a UPI pin. The UPI Id and Pin authenticate all transactions you do on the platform. A UPI Id is usually your mobile number followed by the ‘@’ symbol. It ends with the name of the app you are using or the name of the bank/s that has tied up with the UPI application. Your UPI Id can also be your name. The ID is set up by entering bank account details on the app. The app then sends an OTP to your registered mobile number to make sure that you are an authorised person. On entering the OTP, you will be directed to create a PIN for the UPI ID. Upon completing the registration, you can begin transacting with all those in your contact list having a UPI account.

How safe is UPI?

For a successful transaction to take place, UPI uses a two-factor authentication method. The NPCI claims the UPI payment method to be the safest and most secure mode of payment.

When it comes to considering the economic frauds occurring in the country, there are barely minimum frauds related to UPI recorded in India. As of 2021, the Reserve Bank of India (RBI) reported a total of around 7,400 bank fraud cases across India.

During a conversation with the Police Sub Inspector (who has chosen to stay anonymous) of Cyber Police Station Pune, on the safety of UPI, he said that although the economic frauds in India are high, those resulting from UPI payments are close to zero. He said that the UPI mode of payment is 100% safe. One only needs to know the right ways of using the platform. He added that since all the payments are either done using a QR code or a mobile number and a pin number, there is very less chance of any fraud occurring on this platform.

What do the statistics and facts state?

UPI has gradually emerged as a primary payment option for a majority of Indians making them less reliant on cash. Experts had predicted that reliance on UPI would further increase tenfold by 2020 and believed that 50 per cent of internet users in India will begin to use digital payments by 2020 as well.

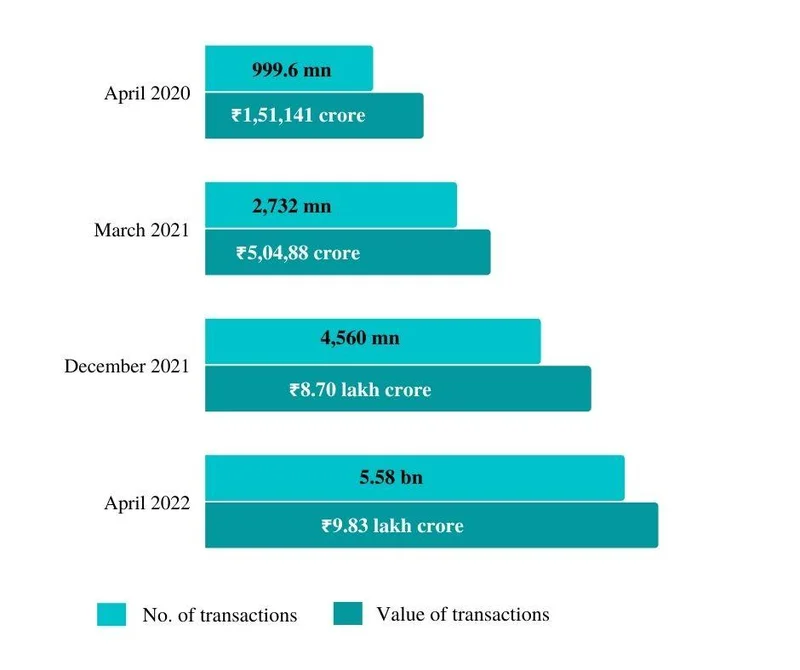

True to this, by March 2021, there were about 2,732 million UPI transactions worth ₹5,04,886 crore as opposed to 999.6 million transactions in April 2020 with the total value of transactions at ₹1,51,141 crore. Two of the main reasons why this rise in UPI transaction was the sharp drop in second wave cases and the festive season like Diwali in India. During this time, Indians shopped in huge numbers after undergoing almost one whole year of lockdown. E-commerce websites and applications like Amazon, Zomato and Swiggy made heavy use of UPI to receive payments from the customers.

Since 2020, UPI has recorded a threefold increase in both the number of transactions and the value. By December 2021, Unified Payments Interface hit a record high of 4,560 million transactions worth Rs 8.70 lakh crore.

As of April 2022, 5.58 billion transactions were carried out through Unified Payments Interface (UPI). This happened to become the highest number of monthly UPI transactions ever since the launch of this digital payments system in 2016. The platform recorded transactions worth ₹9.83 lakh crore in April 2022.

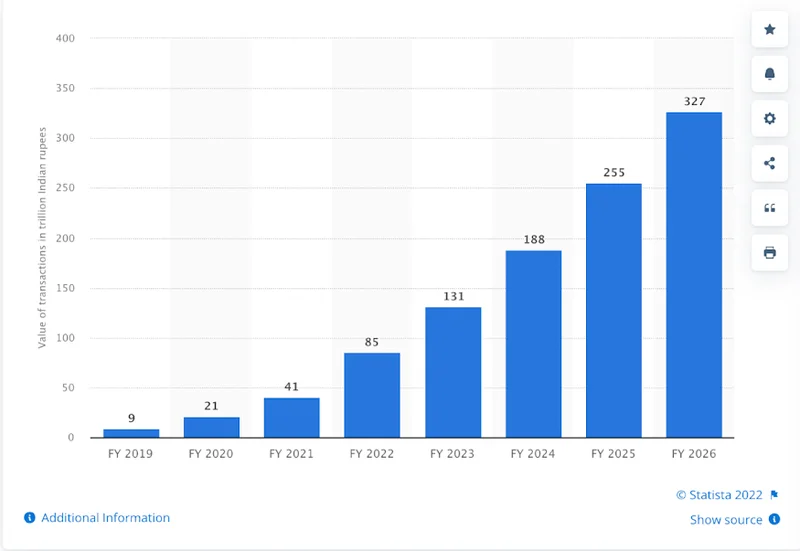

According to Statista, the transaction value is estimated to rise up to over 327 trillion Indian rupees in the financial year 2026 in India.

‘Value of Unified Payments Interface (UPI) transactions in India from the financial year 2019 to 2021, with estimates until 2026 (in trillion Indian rupees)’

Since the launch of UPI in 2016, the number of banks collaborating with the platform to enable transactions has also increased. At its nascent stage, there were only 21 banks on board. Further, in 2020 the number rose to 153 banks and 216 in 2021. Presently there are about 304 banks in India that have gone live on the platform.

Who are the major players on UPI?

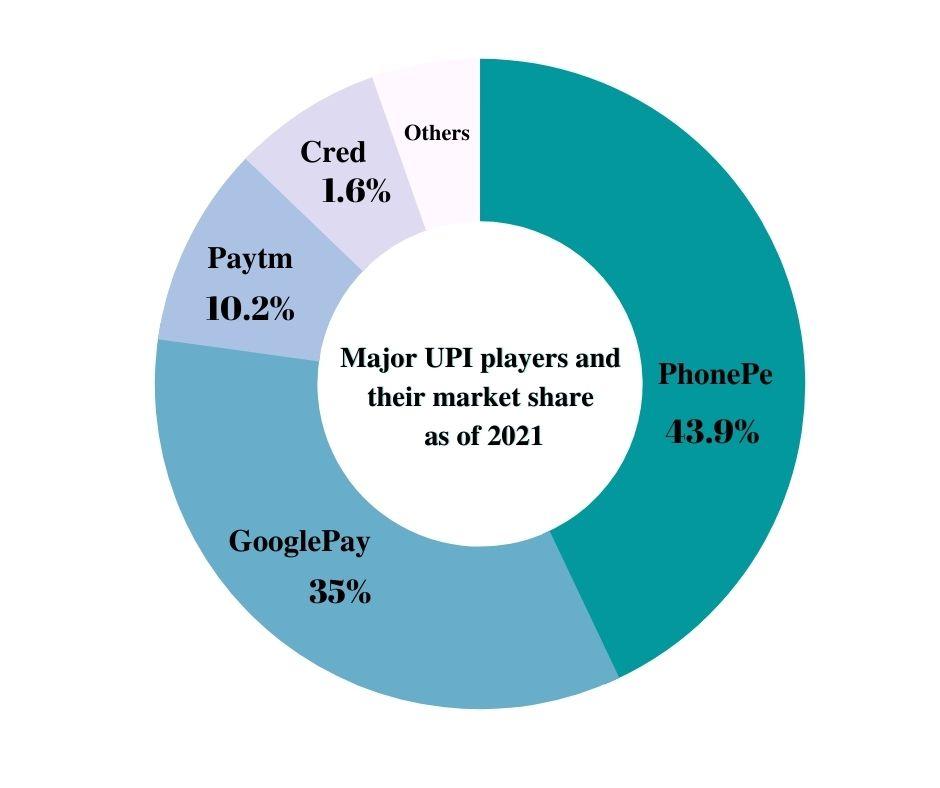

There are two leading players that dominate the UPI market to date. They are Walmart-owned PhonePe and Google Pay. As of 2021, PhonePe contributes to 43.9% of the total UPI transactions volume, recording 1,199.51 million transactions, with a value worth ₹2,31,412 crore. Google Pay on the other hand enjoyed a 35% market share in March, with 957.01 million transactions worth ₹2,01,185 crore. Paytm Payments Bank was the third-largest player, having 401.16 million transactions worth ₹43,221 crores.

Another Indian mobile payments app based on UPI and developed by the NPCI itself, Bharat Interface for Money (BHIM), too, has seen a growth in transactions. The app reported around 14 million transactions (at a value of ₹4,504 crores) in April 2020, and 24.4 million (₹7,653 crores) in March 2021. Cred, another UPI app, has also reported a fivefold growth from 0.94 million transactions (672 crores) to 4.96 million (₹5,390 crores) in March 2021.

What about that limited population of India that still can’t afford to buy smartphones?

To make UPI payments more inclusive for every Indian, keeping in mind that a limited number of the population still can’t afford smartphones, NPCI has facilitated UPI payments without a mobile phone. This is done to bring about social and financial inclusion and to support those who do not own smartphones with the Bharat Interface for Money (BHIM) Aadhaar Pay feature. The BHIM app is primarily a UPI app available in several Indian languages. The app introduced a feature called BHIM Aadhaar Pay under which merchants can receive payments with their Aadhaar number and the biometric information of the customer. This makes possible payments over the counter at any merchant or trader who uses the BHIM Aadhaar app using Aadhaar authentication.

As one more step forward in making UPI payment method accessible to feature phone users, the RBI, very recently, launched a new UPI service named 123PAY. It aims at helping 40 crore feature phone users make digital payments easily without an internet connection. This feature will enable users to make payments in majorly four ways – calling an interactive voice response (IVR), using app functionality in feature phones, proximity sound-based payments and through a missed call functionality.

What does 2022 have in store for UPI in India?

Although UPI is taking a front seat rapidly in the country, many finance and banking pundits believe that the older demographic will continue using debit and credit cards as they find them to be more secure and safe. This is due to the years-long belief in those modes of digital payments.

This, again, does not mean that the popularity of the UPI system will collapse. Cards will continue to lose preference given that UPI is replacing not just cards but cash. The convenience of customers is at the heart of UPI’s future.

Considering the current scenario, the National Payments Corporation of India (NPCI), is aiming to hit UPI transactions worth $1 billion per day in the coming two to three years’ time.

Besides, given the fact that the RBI’s decision to hike the UPI transaction limit to Rs 5 lakh, achieving the 1 billion a day target, doesn’t seem to be very far and is most likely to see the light of the day by December 2022.

A.P. Hota, former managing director and CEO of NPCI has said, “As the name suggested, UPI was considered to be a unifying force. When we started it, our target was to get an active customer base of 500 million. It is nearly 200 million as of now.”

This form of UPI explosion will drive India from being a cash-driven economy to a cashless economy real soon.