Congratulations! You got your first paycheck. Now meet its less popular roommate: income tax.

What Is Income Tax?

Income Tax is basically a tax on your income. It is directly levied by the government to fund public services like healthcare, infrastructure and education. The tax is calculated based on taxable income, and the taxpayers are expected to file an annual return. There are two types of taxes: Direct Tax & Indirect Tax.

Direct Tax Vs. Indirect Tax

Direct tax is what a person or an organisation pays directly to the government. Example: Income Tax, Corporate Tax, and Capital Gains Tax. Indirect taxes are collected by intermediaries like retailers or service providers and then passed on to the government. Example: GST, Custom Duty and Excise Duty.

Why The Government Collects Taxes

The main purpose of tax collection by the government is to fund public services like the construction of roads, schools, hospitals and public transportation. Tax funds are also used for national security, defence, legal and justice systems. Apart from this, taxes help with economic stabilisation and redistribution of wealth.

Why Should You Care About Income Tax?

Why Filing Taxes Matters

Every financial year, as per the annual budgeting announcements, a figure for non-taxable income is finalised by the government. Anything above that becomes taxable. As citizens, it is our duty to rightfully pay taxes after calculating and filing the income tax. This is necessary because it allows us to claim refunds in case someone has mistakenly paid more tax than required.

Benefits Of Filing Taxes Even If You Owe Little Or No Tax

Filing Income Tax Returns also works as a standardised strong proof of your consistency in income, which is very important while applying for visas. They also work for banks when applying for home or other types of loans. ITR filings aid in carrying forward losses so that they can offset future taxable profits and reduce tax liability. It creates a significant financial footprint.

With less income, when you are sure that there is a minimum of taxes to be paid, ITR filing is still beneficial. Banks or employers often deduct taxes before handing out salaries. Filing ITR is the only way to claim it back. At any point in time, the application for loans gets faster if you can provide consistent income proof for 2-3 years. While travelling abroad for educational or other purposes, embassies of many countries consider ITR filing as proof of your income stability.

Common Myths About Taxes

Most people have a misconception that if their income is under the taxable limit, they are not required to file returns. That is a myth. There is a false belief that an increase in income will raise taxes and reduce earnings. But that is not true. Tax systems use marginal tax rates. This means that taxes levied on your income before the promotion remain the same even after getting the raise. The tax levied on the difference amount after deducting the old salary amount from the new salary amount is higher.

Example: You earn ₹1000 and pay a tax of ₹100 [10%] on it. When you start earning ₹1100, you will pay ₹120 as tax. How does this happen? Here’s how. When you earn ₹1100, your ₹1000 still falls under the 10% tax category. The raised ₹100 increment falls under the 20% tax category. So 20% of that and the 10% front he old, adds up to ₹120.

Some people also believe that all monetary gifts are tax-free, but some gifts from distant relatives, up to a certain limit, are taxable. Filing Extension is not extra time to delay payment; if you have to pay, it is best to do it quickly rather than suffer penalties.

Who Needs To Pay Income Tax?

Taxable Income

Any individual earning a salary or running a business, and also non-residents, is liable to pay taxes. The tax is charged on incomes of five major types: salary, business or profession, income generated from rent of owned house property, capital gains from shares or real estate, or other incomes like lottery winnings.

Residents & Non-residents

To get classified as a resident in India, you have to spend more than 182 days or more in one financial year in the country. You can also be classified if you spend 60 days or more in the current year and 365 days or more in total in the preceding 4 years. For a PIO [Person of Indian origin] earning more than ₹15 lakhs visiting India, all the rules remain the same, except that the 60-day or more period changes to 120 days or more. If the person does not meet these criteria, they are non-residents.

India charges tax to its residents on their global income. Whereas there are a few exemptions for the non-residents. Non-residents are only taxed upon income earned, accrued or received within India. Unlike residents, they don’t have a rebate. Residents have an amount up to which their income is not taxable, but non-residents have to pay taxes from the starting slab. While Residents are required to report on accounts and properties from all over the world, non-residents are exempt from this rule. Once you are a non-resident, you have to change your bank account to avoid penalties from the Foreign Exchange Management Act [FEMA].

Salaried Employees, Freelancers & Business Owners

Salaried employees pay taxes on their fixed incomes through their employers, inclusive of taxes on bonuses and allowances. They have a few statutory deductions. Freelancers have to pay taxes on their net profit and not the total revenue. It is calculated by deducting business expenses from gross receipts. It is governed by the Profits and Gains of Business or Profession (PGBP) rules. They can also claim deductions on laptops, office furniture and vehicles.

Taxes paid by business owners vary depending on the type of business. If you are a sole proprietor, the business income is added to your personal income and taxed as per that slab [30%]. If it is a company or LLP, the tax is about 15-30% depending on the type of business. Businesses also pay GST on the tax they collect from customers if their yearly sales for services cross ₹20 lakhs or their yearly sales for products cross ₹40 lakhs. However, this threshold is only applicable in some states and changes as per region. Businesses also pay 1-10% to the government directly on payment to vendors, contractors, or landlords, slicing off from their payment.

How Does Income Tax Work?

Tax Slabs

Tax slabs are specific income ranges set by the government. Every income range as a percentage of tax. It grows with the increase in income. Individuals are required to pay taxes based on their income slab. For this, they can either use the default new tax regime or the old tax regime.

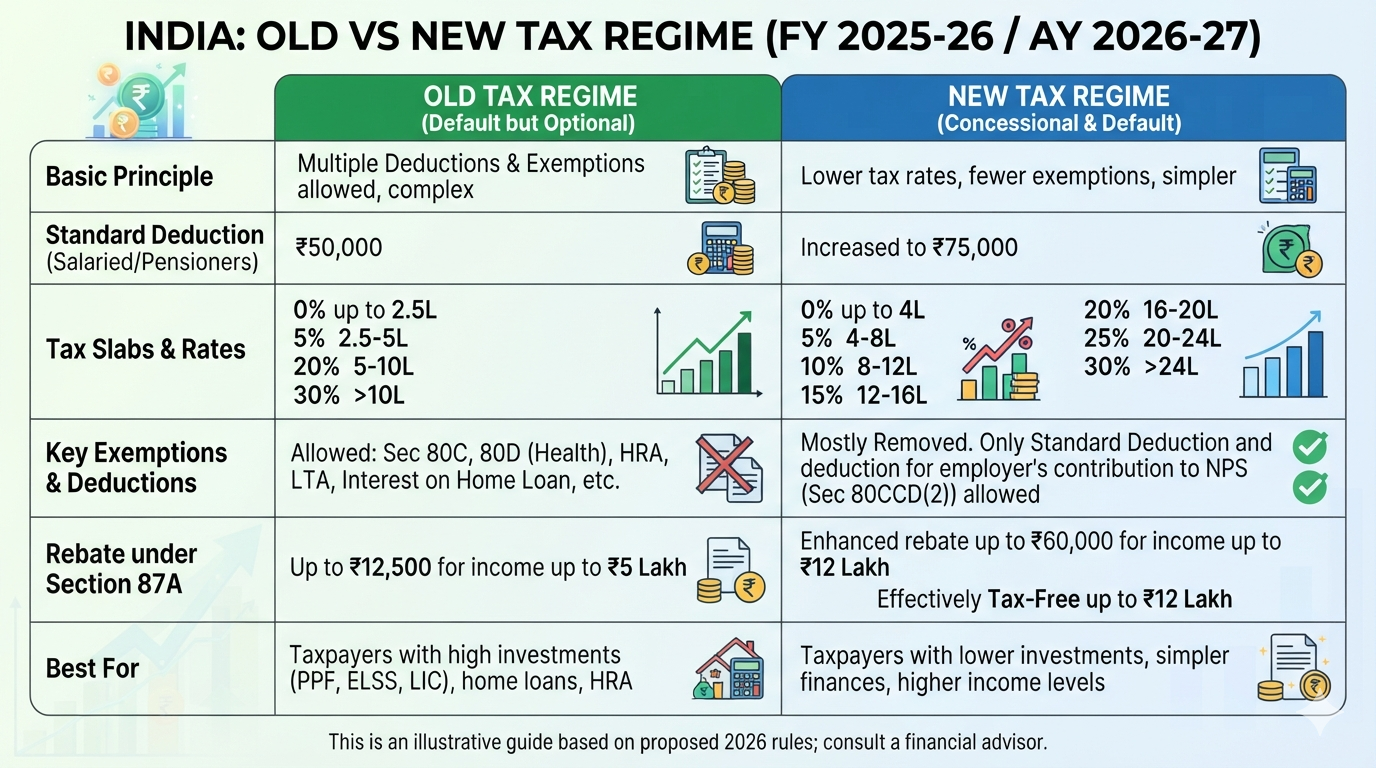

Old Vs New Tax Regime

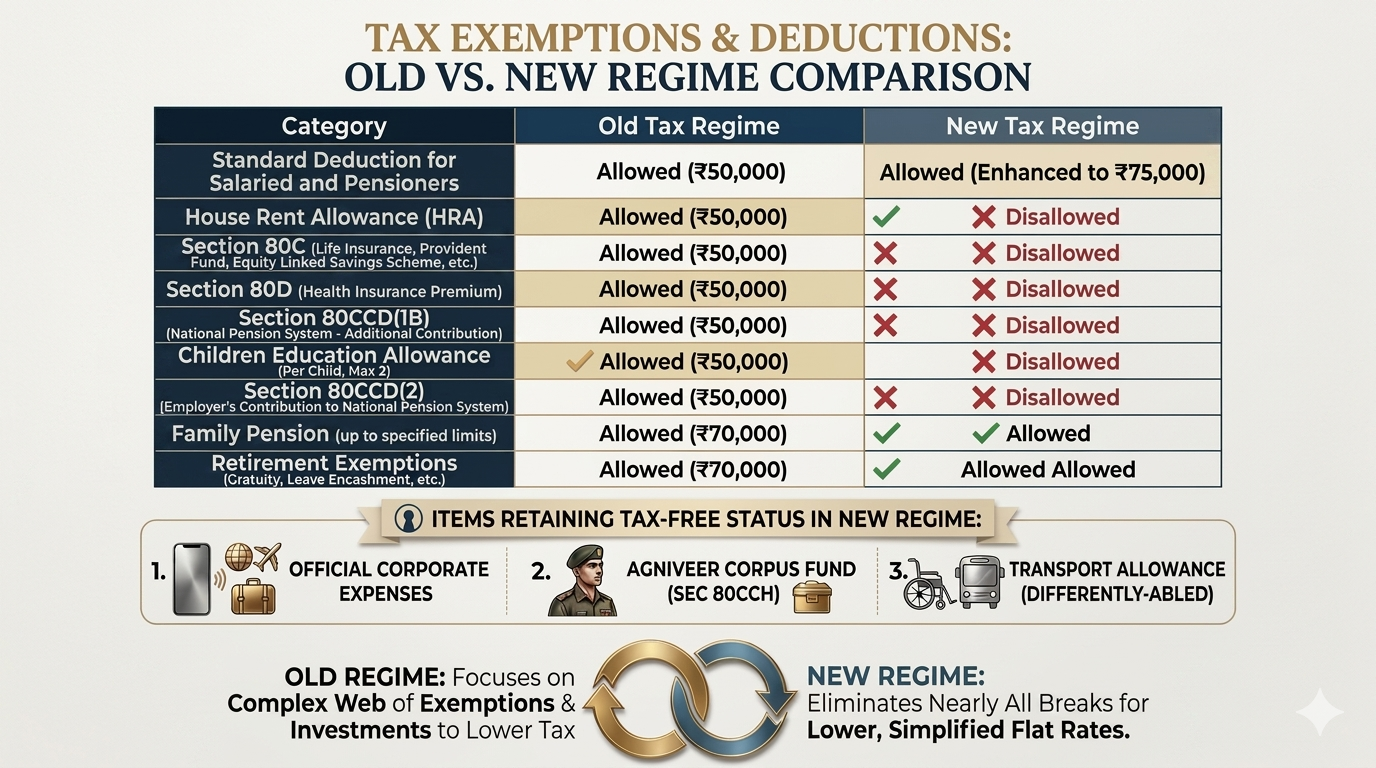

Deductions And Exemptions

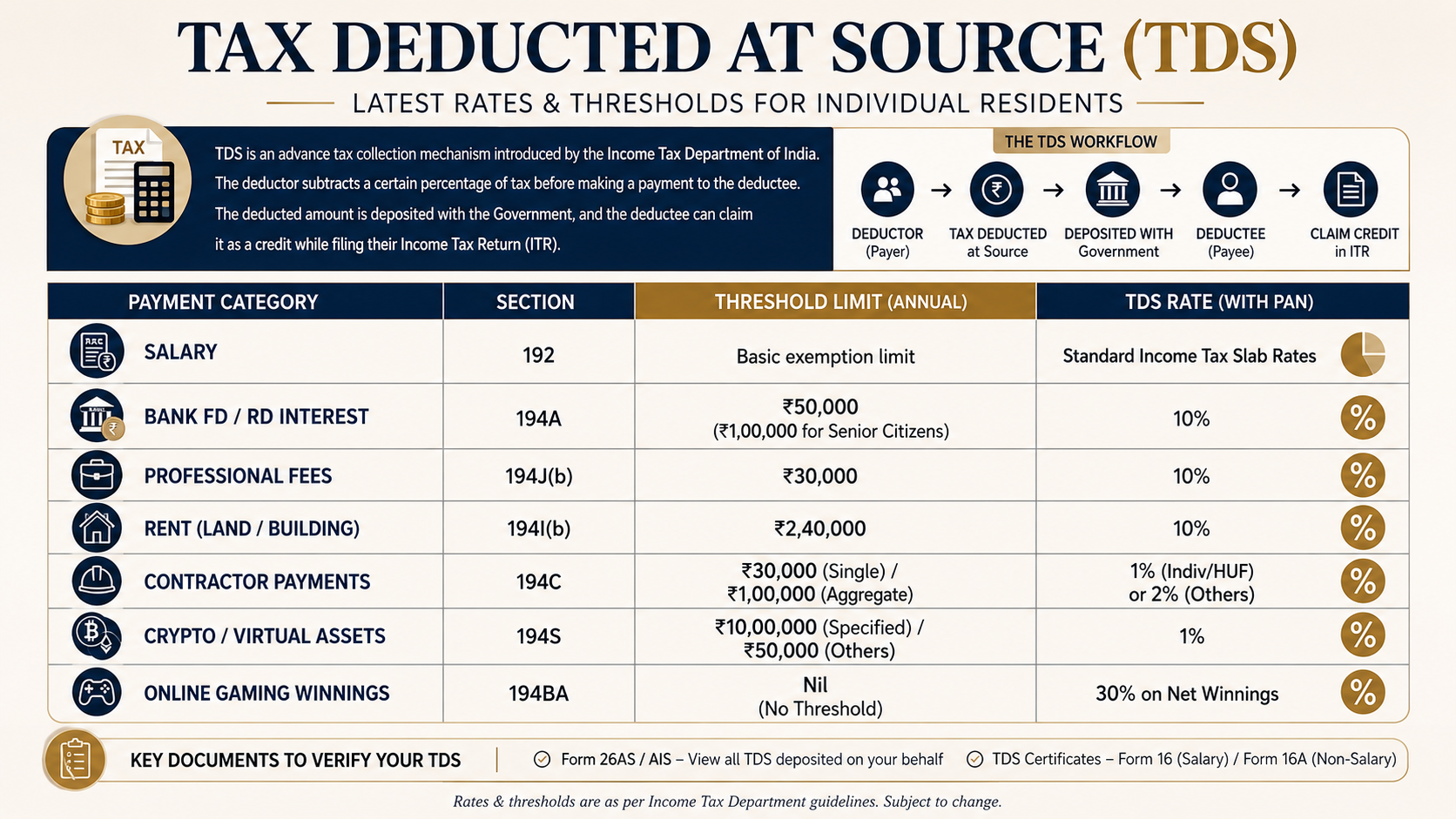

TDS

As commonly heard, Tax Deducted at Source [TDS] is an advance tax collection system introduced by the Income Tax Department of India. The person or the company making a payment gets to deduct a specific amount from it [tax percentage] before giving the amount to the receiver. The deducted amount is directly deposited with the Central Government, and the receiver can claim it as a credit against annual tax liability while filing returns.

Documents Required For Filing Income Tax Returns

Basic documents like the PAN card and Aadhaar card are required for filing, along with Income Statements like Form 16. You can verify your tax credits using Form 26 AS. You can get your Annual Information Statement [AIS] through the Income Tax E-filing Portal.

Basic Identification Details

PAN card linked with Aadhaar card

Aadhaar card

Bank details, including bank statements for the financial year

Income Verification Documents

Form 16 issued by the employer

Monthly salary slips

Interest certificates from banks/post offices

Capital Gains Statements

Rental Income documents like agreements and municipal tax receipts

Tax Credits & Deduction Documents

Form 26AS & AIS from the Income Tax India TRACES Portal

Receipts for investments under section 80C[Investment Proof]

Receipts for health insurance premiums, education loan interest and housing loan interest certificate[Deduction Proof]

Rent receipts for HRA claim [if rent exceeds 1 lakh rupees per year, with the PAN Card of the landlord]

How To File Your Income Tax Return in 2026?

Gather all the documents

Log in to the Income Tax E-filing Portal

Navigate and choose the correct year and online mode for filing

Select the applicable category and form [ITR-1 for salaried individuals and ITR-3 or ITR-4 for business or professional incomes]

Review pre-filled data and select your tax regime

Submit after a thorough review and e-verify via Aadhaar OTP, net banking or bank account.

Common Mistakes To Avoid While Filing Income Tax Returns

Do not choose the wrong assessment year [Ex: for FY 2025-26, the assessment year is 2026-27]

Do not ignore Form 26 AS or AIS, as it registers as mismatched information

Choose the correct ITR form

Do not skip exempt income

Include all bank accounts

Pre-validate the account for refund, no wrong IFSC codes

Do not forget to E-verify

Do not miss the filing deadline

Tax Planning Tips

Always make sure that you are not doing things the night before. Be prepared. Get your hands on all the documents before the deadline. Keep a digital record of all the required documents and statements. Understand your salary structure and compare tax regimes well. Review your tax regime annually to stay ahead. Take advantage of sections 80C and 80D. Utilise home loan benefits and take advantage of the National Pension System. Do not forget to review your mid-year tax statements.

Kids, adults and senior citizens all get taxed differently in all categories. Make sure that you are aware of all the rules and regulations. It is beneficial to file your tax return, unlike people claiming otherwise. Try it, and you will know. Keep your finances in your hands